Understanding HOA Reserve Funds: A Plain-Language Guide for Boards

Most HOA board members didn't sign up to learn financial accounting. They volunteered because they care about their community, and the role came with a stack of governing documents, a budget spreadsheet, and an annual reserve study that uses language they didn't expect to need. The treasurer might have a finance background. The rest of the board usually doesn't.

This guide is the plain-language reference. What HOA reserve funds actually are, why they matter, how the reserve study connects to the budget, and what the board should know to ask the right questions — without needing to learn accounting from scratch.

What reserve funds are, in one paragraph

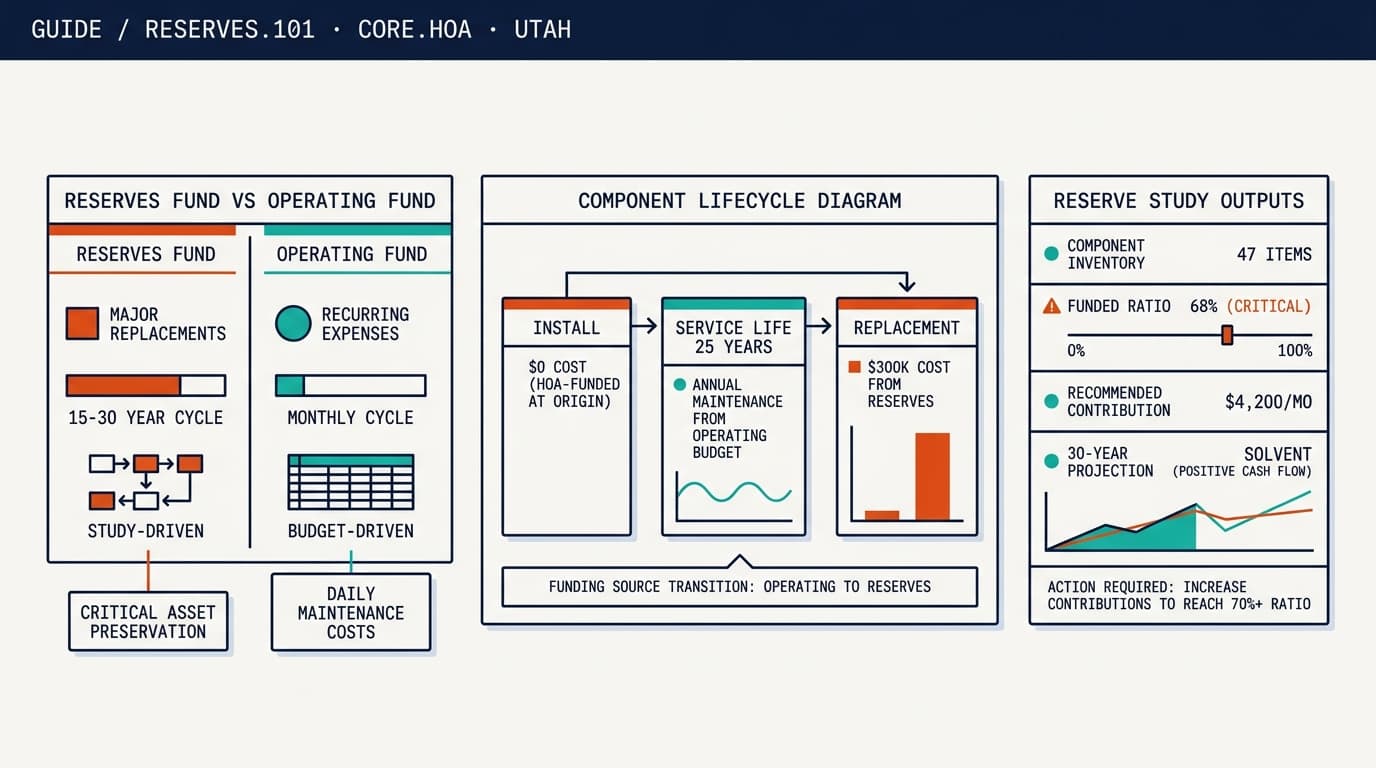

Reserve funds are money set aside in a separate account to pay for major component replacements over the building's life cycle. Roofs, asphalt, mechanical systems, exterior painting, elevators, pool resurfacing — anything that has to be replaced periodically and costs more than routine operating expenses can absorb. The reserve account is funded by monthly contributions from homeowner dues, sized by a reserve study so the money is available when the components reach end-of-life. Without reserves, replacements get funded by special assessments — emergency dues hits to homeowners — which are politically painful and financially disruptive.

That's the whole concept. Everything below is detail.

Why reserves exist (and why most HOAs underfund them)

Major components in any building have predictable lifespans. A composition shingle roof lasts 20-25 years. Asphalt parking lot pavement lasts 15-20 years. Boilers, HVAC systems, and water heaters last 15-25 years depending on the equipment. Exterior paint cycles run 7-10 years. Elevators have major modernization cycles around 25-30 years.

The replacement costs for these components are significant. A roof replacement on a 50-unit condominium can run $300,000-$600,000. A full asphalt replacement on a 100-space parking lot can run $150,000-$400,000. These aren't expenses an HOA can absorb in a normal operating year.

The math problem is straightforward: predictable replacements at predictable intervals require predictable savings. The reserve fund is the savings vehicle.

The reason most HOAs end up underfunded isn't ignorance of the math. It's the political reality of volunteer governance. Past boards faced pressure to keep monthly dues low. They kept reserve contributions modest, often below the levels their reserve studies recommended. The gap compounded. By the time the current board inherits the situation, the underfunding is 10-20 years old and the components are approaching end-of-life.

For deeper analysis on diagnosing underfunding, see How Salt Lake City Boards Can Tell If Reserves Are Underfunded.

How a reserve study works

A reserve study is the professional analysis that turns the abstract concept of "save for replacements" into actual numbers a board can use.

A qualified reserve specialist (typically a licensed reserve study professional, often a CPA or engineer) does five things:

1. Component inventory. Walks the property and documents every major component subject to replacement. Roof sections, parking surfaces, mechanical equipment, painting surfaces, elevators, pool equipment, fencing, signage. Each component gets identified, located, and described.

2. Condition assessment. Evaluates the current condition of each component. A 12-year-old roof in good condition has different remaining life than a 12-year-old roof showing wear. The condition assessment refines the useful-life estimate.

3. Useful-life and remaining-life calculation. Estimates how many years each component has before replacement is necessary. Useful life is the standard expected lifespan; remaining life is what's left given current condition and age.

4. Replacement cost estimation. Estimates current cost to replace each component. Inflation factors get applied to project the cost at actual replacement time.

5. Funding model. Calculates the contribution rate needed to fund all replacements without special assessments. Two methods are common — the cash-flow method (smooth contributions over 30 years) and the component method (full funding of each component at end-of-life). Either is defensible if applied consistently.

The output is a document — typically 50-100 pages — that shows the projected replacements, the projected costs, the recommended reserve balance for each year over the next 30 years, and the recommended contribution rate.

How to read a reserve study without a finance background

Most reserve studies are dense documents. Boards don't need to read every page. Five sections matter most.

The Executive Summary

Usually the first 2-5 pages. Summarizes the community's current funded position, recommended contribution rate, and major findings. If you read nothing else, read this.

Look for:

- Funded ratio as of the study date (the percentage of recommended balance currently held)

- Recommended monthly or annual contribution for the upcoming year

- Major findings — components in poor condition, replacement projects in the next 1-3 years, any surprises

The Component Inventory

Usually a table or list showing every major component with useful life, remaining life, current condition, and replacement cost. Skim this. The board should be able to recognize the components and verify the remaining-life estimates feel approximately right based on what they know about the community.

If a component the board knows is in bad shape shows "good" condition in the study, that's a flag to discuss with the reserve specialist. The study is only as good as the inputs.

The 30-Year Projection

A multi-page table or chart showing projected reserve balance, contributions, and disbursements year by year for 30 years. The key visual is whether the projected balance stays positive across the entire timeline. If the line dips below zero in any year, the funding plan doesn't work and either contributions need to increase or replacement timing needs to shift.

The Funding Recommendation

Usually 1-2 pages. States the recommended contribution rate explicitly. May offer multiple scenarios — current funding, threshold funding, full funding — with the implications of each.

The board's decision is which funding scenario to adopt. The most aggressive scenario (full funding) builds reserves fastest but requires the highest contributions. The least aggressive (threshold funding) maintains a positive balance but leaves the community more exposed to unexpected component failures.

The Disclosures

Usually at the end. States what the reserve specialist included or excluded, what assumptions were made about inflation, what's outside the scope of the study. Read this once to understand the document's limitations.

What the reserve fund should and shouldn't be used for

The reserve fund is for major component replacements as defined in the reserve study. That's it. Specifically:

Yes, reserves cover:

- Roof replacement

- Asphalt sealing and resurfacing

- Exterior painting on the published cycle

- Major mechanical equipment replacement (boilers, HVAC, elevators)

- Pool resurfacing and major pool equipment

- Major fencing or signage replacement

- Other components specifically inventoried in the reserve study

No, reserves should not cover:

- Routine operating expenses (utilities, insurance, management fees, landscaping)

- Minor repairs that fall under maintenance budget

- Project work outside the reserve study's component inventory (typically funded through capital improvements assessment or project-specific funding)

- Unfunded pet projects or board priorities

Mixing reserves with operating funds is a sign of weak financial controls. Some boards do it because the operating account ran short and reserves had cash. The fix is bookkeeping discipline, not informal borrowing from reserves. When reserves get used for non-reserve purposes, the funded ratio drops and the underfunding compounds.

Reserve study timing and refresh cadence

A reserve study should be:

- Commissioned at community formation if developer-built, or as soon as practical if that step was missed

- Updated every 3-5 years with a full inventory walkthrough and condition reassessment

- Reviewed annually as a desk update — checking whether component costs have moved by more than 10%, whether any conditions have changed materially, whether assumptions still hold

The full update costs $2,500-$6,000 for a typical Utah condominium community. Larger or more complex communities cost more. The cost is small relative to the consequences of operating without current data.

Communities operating from a study more than five years old are operating from data that doesn't reflect current replacement costs. Cost inflation since 2020 has been particularly aggressive in construction and mechanical equipment categories. A 2019 study underestimating 2026 replacement costs by 30-40% is plausible.

Three actions for any board reading this

Three things every board should do this quarter regardless of community circumstances:

Action 1 — Find the reserve study. Locate the most recent reserve study for the community. If the most recent is more than three years old, schedule an update. If there's never been one, commission the first one.

Action 2 — Calculate the current funded ratio. Pull the current reserve balance and divide by the recommended balance from the study. The percentage tells you where the community stands. Below 70% is underfunded. Below 30% is in the danger zone.

Action 3 — Review the contribution rate. Compare what the budget contributes to reserves against what the study recommends. If contributions are below the recommendation, the gap is widening every month.

These three steps take less than a board meeting to complete and produce more financial clarity than most boards have ever had.

How Core HOA approaches reserves

Reserve work at every Core HOA-managed community runs on a continuous rhythm. The reserve study is current — typically refreshed every three to five years with annual desk reviews between full updates. Funded ratios appear on the board cockpit in real time. Contributions get tracked monthly against the reserve study's recommended rate. Drift gets surfaced before it becomes a board agenda item.

This is what continuous financial intelligence does for reserves. The reserve study isn't a document that sits in a drawer between annual meetings — it's a living model that informs every budget decision the board makes. Drift caught at the rhythm, not at the failure.

Frequently asked questions

What are HOA reserve funds?

HOA reserve funds are money set aside specifically to fund major component replacements over the building's life cycle — roofs, asphalt, mechanical systems, exterior painting, elevators. Reserves are separate from operating funds, which pay for routine ongoing expenses. The reserve account is funded by monthly contributions sized by a reserve study to cover replacements when components reach end-of-life.

What is a reserve study?

A reserve study is a professional analysis that inventories every major component in a community, estimates remaining useful life, projects replacement costs, and calculates the contribution rate needed to fund replacements without special assessments. Reserve studies are typically conducted by qualified specialists and updated every three to five years to reflect changing costs and component conditions.

Are HOA reserve studies required in Utah?

Utah does not currently require reserve studies for most HOAs by statute, unlike states such as California or Washington. However, lender requirements for FHA-approved condominium associations and prudent fiduciary practice both effectively require them. Boards operating without current reserve studies are operating without the data needed to meet their fiduciary duty.

How often should an HOA update its reserve study?

Industry guidance from organizations like CAI recommends updating reserve studies every three to five years. The cadence balances cost (a full update costs $2,500-$6,000) against accuracy (component costs and conditions change continuously). Some firms recommend annual desk reviews between full updates to catch significant changes early.

What's the difference between operating funds and reserve funds?

Operating funds pay for routine, ongoing expenses — landscaping, utilities, insurance, management fees, minor repairs. Reserve funds pay for major component replacements that happen on long cycles — roofs, asphalt, mechanical systems. The two should be in separate bank accounts with separate accounting. Mixing them is a sign of either sloppy bookkeeping or worse.

Questions about your reserve position?

If your board wants a structured review of your community's reserve position and what recovery would look like, request a proposal. We'll send the math, not the marketing.

This article was prepared by the Core HOA Editorial Team based on standard practice in Utah HOA management. For community-specific reserve guidance, contact Marc directly at marc@corehoa.com.