The HOA Budget Build: A Treasurer's Annual Walkthrough

The HOA budget is the single most important financial document a board produces in a year. It funds everything — operations, maintenance, reserves, professional services, every vendor invoice the community will pay over the next twelve months. Done well, it sets the community up for a year of stable operations and steady reserves growth. Done poorly, it locks in an underfunded position the board will spend the rest of the year managing around.

Most HOA treasurers inherit a budget process rather than design one. The board chair hands over a spreadsheet from last year, says "bump the numbers," and the new treasurer adjusts line items by gut feel under time pressure before the December board meeting. The result is a document that looks like a budget but doesn't function as one — no real model behind it, no clear connection to the reserve study, no defensible math when homeowners ask why dues went up.

This guide is the structured walkthrough. How a Utah HOA treasurer should build the annual budget from scratch — the calendar, the stages, the math at each step, and the specific line items that boards routinely under-build.

Why the budget calendar matters

Most communities operate on a calendar fiscal year — January through December. The budget for the upcoming year needs to be approved by the board before the year begins, ideally with enough lead time to communicate any dues changes to homeowners.

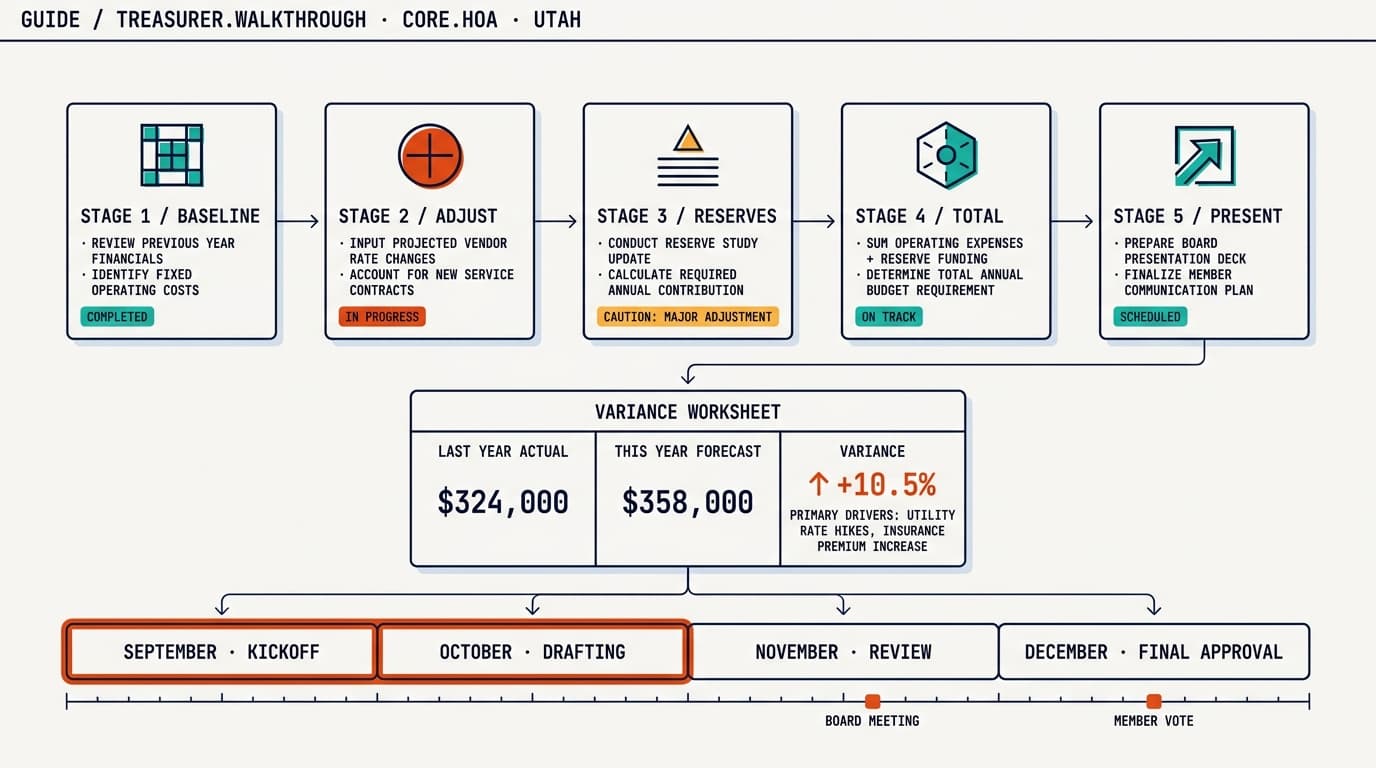

Working backward from January 1, the calendar looks like this:

- September — Pull historical data, run reserve study refresh, begin line-item review

- October — Complete first-draft budget, circulate to board for input

- November — Refine draft based on board input, finalize reserves contribution

- December — Board approves budget, communications go to homeowners

- January 1 — New fiscal year begins under approved budget

A community that starts the budget process in November is already behind. A community that starts in December is improvising. The math doesn't change but the quality of the work does — every stage compressed produces compromises that show up later as variance.

The five stages of a defensible budget build

Stage 1 — Pull the historical baseline

Start with last year's actuals, not last year's budget. Actuals show what the community actually spent. Budget shows what the prior treasurer thought the community would spend. The variance between them is the signal.

Pull a 12-month report of every expense line. Group by category:

- Management fees and administrative expenses

- Utilities (water, sewer, gas, electric, trash)

- Insurance premiums

- Maintenance (recurring and project-based)

- Landscaping and grounds

- Professional services (legal, accounting, audit)

- Reserve contribution (last year's actual transfer to reserves)

- Other (technology, communications, board expenses)

For each line, note the year-over-year change. A line that was $24,000 in 2024 and $31,000 in 2025 is showing a 29% increase that needs an explanation before it gets carried into 2026's baseline.

Stage 2 — Adjust line items for known changes

The historical baseline tells you what last year cost. The 2026 budget needs to reflect what 2026 will cost — with adjustments for known changes.

Run through each line and ask:

Inflation adjustments. Most expense categories are seeing 4-8% annual cost increases in the current Utah market. Apply a category-specific inflation factor rather than a flat percentage — utilities are running higher, professional services are running closer to standard CPI.

Vendor contract changes. Any vendor whose contract is renewing in the budget year should be projected at the new contract rate. If the vendor hasn't quoted yet, project conservatively (high) and revise when the actual rate arrives.

Insurance premium changes. Insurance markets have hardened across Utah HOAs in the last 24 months. Premium increases of 15-30% are common at renewal. The treasurer should get a preliminary renewal indication from the broker before finalizing the insurance line.

Project-driven expenses. Major projects approved by the board for the budget year — exterior painting, asphalt sealing, roof replacement, mechanical system upgrades — go on the budget at vendor-quoted prices. If the project requires reserves draw, the budget should show the operating-side impact (project management, communications, etc.) separately from the reserves draw itself.

One-time vs. recurring. Last year's budget may have included one-time expenses that don't repeat in the new year. Strip them out. Conversely, new recurring expenses (a new vendor relationship, a new technology subscription) should be added.

Stage 3 — Model the reserves contribution

The reserves contribution is the most consequential single line item in the budget. It's also the line item most commonly underfunded.

The contribution should be calculated from the community's current reserve study, not from gut feel or last year's contribution rolled forward. Reserve studies use one of two methods:

Cash-flow method. Calculates the annual contribution needed to maintain a positive reserve balance over the next 30 years given projected component replacements. Produces a smooth contribution that funds the reserve over time.

Component method. Calculates the annual contribution needed to fully fund each component's replacement at end-of-life. Produces higher contributions but a more conservative reserve position.

Most Utah communities run the cash-flow method. Either is defensible if applied consistently.

The treasurer's job at this stage:

- Confirm the reserve study is current (within the last three years; ideally within the last year for an updated funding analysis).

- Pull the recommended contribution for the budget year from the study.

- Compare to the prior year's actual contribution.

- Identify any gap and make a recommendation to the board.

Communities consistently contributing less than the reserve study recommends are running an underfunded position by definition. The treasurer's role isn't to advocate for higher contributions for political reasons — it's to surface the math so the board can make an informed decision.

For deeper analysis on diagnosing reserve underfunding, see How Salt Lake City Boards Can Tell If Reserves Are Underfunded.

Stage 4 — Calculate total budget and required dues

With expenses adjusted (Stage 2) and reserves contribution modeled (Stage 3), the budget total falls out:

Total budget = Adjusted operating expenses + Reserves contribution + Contingency

Contingency is the buffer for unforeseen expenses. Typical contingency runs 3-5% of total operating expenses. Lower contingency in stable communities with predictable cost patterns; higher contingency in aging communities or those with deferred maintenance backlogs.

From the total budget, the required monthly dues fall out:

Monthly dues per door = (Total budget − Non-assessment income) ÷ (Number of doors × 12)

Non-assessment income includes interest earned on reserves, late fees collected, and any other income (clubhouse rentals, vending revenue). For most Utah HOAs, non-assessment income is small relative to total budget — maybe 1-3%.

The required monthly dues number is the answer to the most important question the board will face: do dues need to increase, and by how much?

Stage 5 — Present to the board with variance analysis

The budget presentation to the board should include:

The headline number. Total budget, required dues per door, percentage change from prior year. Lead with this.

Line-by-line variance from prior year. Every line should show prior year actual, current year budget, and percentage change. Lines with material changes (>10% in either direction) should have a one-sentence explanation.

Reserves position. Current funded ratio, projected funded ratio at end of budget year, and the reserve study's recommendation. If the budget contributes less than the study recommends, surface the gap explicitly.

Sensitivity analysis. What happens if insurance comes in 10% higher than budgeted? What if a major project hits unexpectedly? The budget should be defensible at one or two stress points, not just at the base case.

Recommendations. The treasurer's recommendation to the board on dues, contingency, and any extraordinary actions (special assessment, dues increase phasing, capital reserves loan).

A budget presented this way is defensible at the homeowner meeting that follows. A budget presented as just a spreadsheet with adjusted numbers is harder to defend the moment a homeowner asks "why did dues go up?"

The line items boards routinely under-build

Three line items are systematically underestimated in self-built HOA budgets. Worth flagging explicitly.

Reserves contribution

Discussed at length above. The most common single source of long-term financial trouble in HOAs. Boards under-contribute to keep dues low; the gap compounds; eventually a special assessment becomes the only path forward. Treasurer's job is to show the math regardless of the political dynamics.

Insurance

Insurance premiums have been increasing sharply across Utah HOAs since 2022. Communities budgeting at last year's premium rates routinely face 15-30% renewal increases that hit mid-year and blow up the budget. Best practice: get a preliminary renewal indication from the broker before finalizing the budget, and budget toward the upper end of the indication.

Professional services

Legal review, audit, reserve study refreshes, and specialized consulting work tend to get under-budgeted because they're irregular. A community that doesn't have a reserve study refresh in this year's budget is deferring it to a future year. A community that doesn't budget for an audit will skip the audit. The lines should be present with realistic numbers even if the work is intermittent.

How a management firm changes the budget process

A community with professional management runs the budget process differently from a self-managed community. The management firm:

- Provides historical data in structured format (no manual extraction from QuickBooks)

- Applies inflation factors and vendor adjustments based on portfolio-wide knowledge

- Models reserves contribution against the reserve study automatically

- Produces variance analysis as a standard output, not as a special request

- Drafts the board package and homeowner communications in templates that have been used across many communities

The treasurer's role shifts from spreadsheet-builder to budget-reviewer. The math is still the treasurer's responsibility — the math just gets surfaced by a system rather than constructed manually under time pressure.

For self-managed communities, the budget process is harder but not impossible. The framework above runs in any community. The volunteer treasurer just has to allocate the time, which is the dimension most often missing.

How Core HOA approaches the budget cycle

Budget cycles at every Core HOA-managed community run on the same calendar. September data pull, October draft circulation, November board input, December approval, January implementation. The reserves contribution is modeled against the current reserve study and presented to the board with a funded-ratio trajectory. Variance analysis comes standard. Insurance renewal indications get pulled in time to avoid mid-year surprises.

The treasurer at a Core HOA community spends meeting time on strategic decisions — phasing dues increases, evaluating major project timing, prioritizing reserves recovery — rather than on assembling the data the decisions are made from. The data assembly runs on the rhythm. The decisions run on the data.

This is the difference between budget-as-document and budget-as-operating-model. Both produce a spreadsheet. Only one of them produces a community that runs smoothly the year after the budget is approved.

Frequently asked questions

How does an HOA board build its annual budget?

A defensible HOA budget is built in five stages: pull the prior year's actuals as a baseline, adjust each line item for known cost changes and inflation, model the reserves contribution against the current reserve study, calculate the total budget and required dues, and present to the board with variance analysis. The process should run on a calendar — most communities start in September for a January fiscal year.

When should an HOA start its annual budget process?

For HOAs operating on a calendar fiscal year, the budget process should start no later than September. This allows time for line-item review in September and October, draft budget circulation in November, board approval in December, and homeowner notification before the new fiscal year begins. Starting later compresses every stage and forces compromises that show up later as variance.

What should be included in an HOA budget?

An HOA budget includes operating expenses (management fees, maintenance, utilities, insurance, professional services), administrative expenses, contingency, and the reserves contribution. Income side includes assessments, late fees, and any non-assessment income. The reserves contribution is often the largest single line item and the one most commonly underfunded.

How much should an HOA contribute to reserves each year?

The reserves contribution should be calculated from the community's current reserve study using either the cash-flow method or the component method. Most reserve studies recommend annual contributions in the range of 15-30% of total budget, depending on the age of the community and condition of major components. Communities contributing less than 15% are usually underfunding their reserves.

Can an HOA board approve a budget that requires a dues increase?

In most Utah HOAs, the board can approve a budget that includes a dues increase, subject to specific limits in the governing documents. Some CC&Rs cap annual dues increases at a specified percentage; others allow board discretion. Substantial increases or special assessments often require homeowner ratification depending on the community's governing documents and the size of the increase.

Need a structured budget process?

If your board is building budgets in spreadsheets the night before approval and watching variance compound across the year, request a proposal. We'll send the math, not the marketing.

Marc Kennedy is the owner of Core HOA, a family-owned HOA management firm based in Cottonwood Heights, Utah. Core HOA has managed Utah communities for over twenty years across the Wasatch Front. Marc reads every email sent to marc@corehoa.com.