The 10-Question Test: How to Evaluate an HOA Management Company in Utah

Most HOA boards evaluate management firms the same way: three sales calls, three glossy proposals, a vote at the next board meeting, and a contract signed under time pressure. The firm that wins is usually the one with the best closer, not the best operations. Six months later the board is back where it started — different name on the invoice, same response delays and same surprise fees — wondering what they missed.

What they missed wasn't a question of price or personality. It was the operational reality the firm was running. Most HOA management firms can sell well. Far fewer can run well. The gap between selling and running is what costs your community money for the next two to three years until the contract turns over.

The ten questions below are the diagnostic. None of them appear on a sales deck. All of them surface the structural difference between a firm with operational depth and a firm with a polished pitch. Use them in any vendor evaluation — Core HOA included.

Why the standard sales pitch hides what matters

HOA management is sold the way most service businesses are sold: relationship, references, a brochure of capabilities, a tour of the office. None of that tells you how the firm actually operates day to day.

The operational reality of running an HOA management firm is messy. Compliance windows close on calendar dates that don't care about your portfolio size. Insurance renewals stack up in March. Vendor certificates expire mid-project. Statutory filings have hard deadlines and soft enforcement that turns hard the moment something goes wrong. A firm with operational depth has a structured rhythm for tracking all of it. A firm without it has a manager scrambling, a board frustrated, and a series of fires that turn into special assessments.

The standard sales pitch hides which kind of firm is across the table. The ten questions below force the answer into the open.

The 10 questions, with what a good answer looks like

Read these as a board, not as a homeowner. The questions are scoped to the operational reality the firm faces, not to the experience your individual unit will receive.

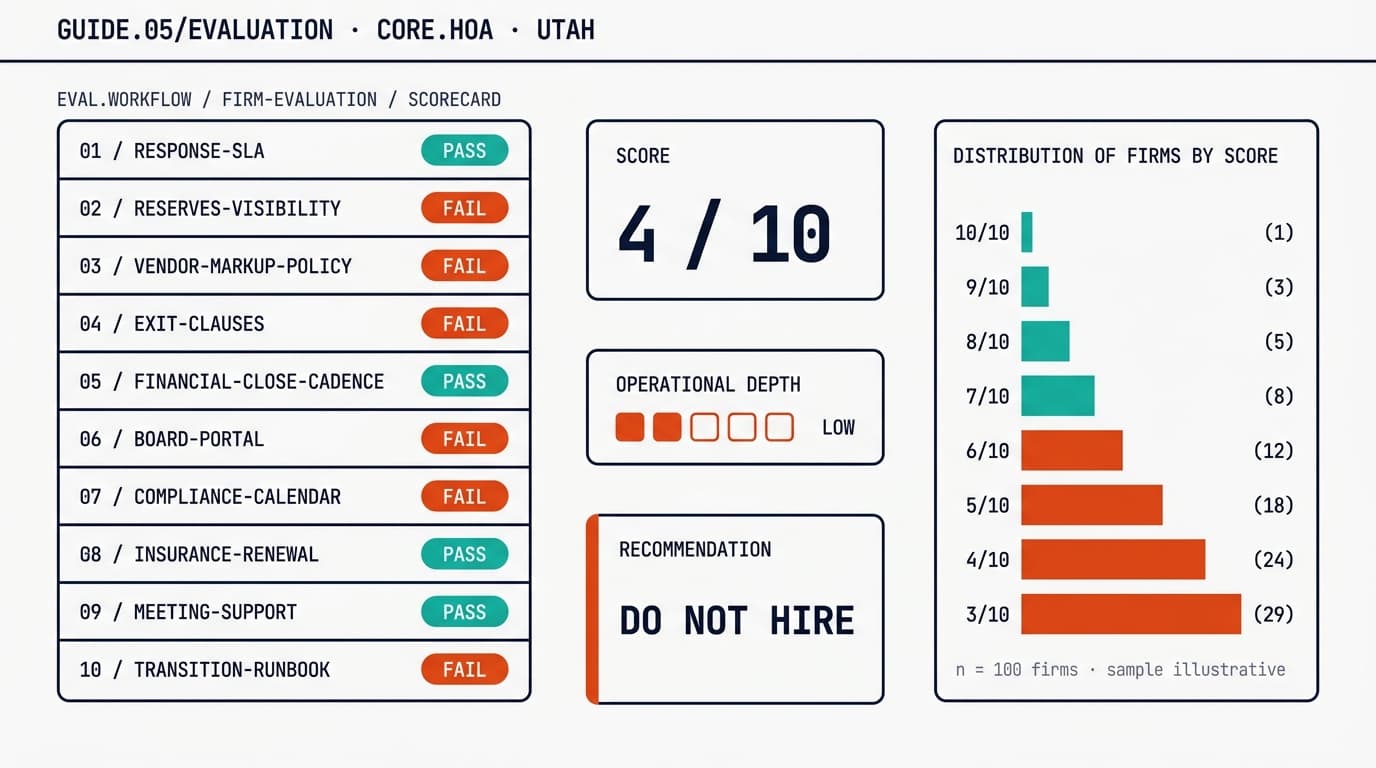

Question 1 — What is your response SLA, and how do you measure it?

A response SLA is a service-level agreement: a published commitment to respond within a defined window. "We're responsive" is not a response SLA. "Same-day response on weekdays for non-emergency homeowner inquiries, two-hour response on emergency dispatch, and twenty-four-hour response on board questions" is a response SLA.

The follow-up question matters more than the first answer: how do you measure it? A firm that tracks response time has logs, dashboards, and a number they can quote. A firm that doesn't track it is improvising and hoping nothing goes wrong.

Good answer pattern: Specific time commitments by category, a tracking mechanism, a willingness to share recent metrics.

Red flag pattern: "We're really responsive" / "Our team prides itself on quick turnaround" / any answer without numbers.

Question 2 — How does your board see reserves projections, and how often do they update?

The reserves question is where most management firms expose how far their financial work actually goes. A firm that sends a static budget once a year and a financial summary at quarterly meetings does not have reserve projection capability. A firm that runs continuous reserve modeling tied to component-replacement schedules and inflation forecasts can show you a live trajectory at any board meeting.

The treasurer is the right person to evaluate this answer. If the firm's reserves work doesn't make sense to a treasurer, the work isn't real.

Good answer pattern: A specific cadence (monthly close, quarterly intelligence review), specific outputs (variance analysis, multi-year projection), specific tools (named software or process).

Red flag pattern: "We work with reserve study consultants" (this means they don't do reserve work — they outsource it once every five years).

Question 3 — What's your vendor markup policy?

Vendor markup is the percentage a management firm adds to vendor invoices before passing them through to the HOA. It can range from zero (the firm passes invoices through at cost) to thirty percent or more (the firm treats vendor coordination as a profit center). Some firms disclose it. Many don't.

The right answer isn't necessarily zero markup — coordination has real cost and a transparent markup is defensible. The wrong answer is any version of "we don't really mark things up" or "it depends on the vendor." A firm that won't put a number on this is hiding something.

Good answer pattern: A specific percentage or a clear pass-through policy, in writing.

Red flag pattern: Evasion, qualifications, or "we'll send you the invoices and you can see for yourself" (which means the markup is buried in the line items).

Question 4 — What does your exit clause look like?

Every management contract has termination terms. Most boards don't read them until they're trying to leave. By then the cost of the exit is locked in.

The questions that matter: How much notice is required? What's the termination fee, if any? Does the firm export your data in a usable format on departure, or do they hold it hostage? Are there setup fees for the next firm because the data export is incomplete or proprietary?

Good answer pattern: Sixty-day notice, no termination penalty, full data export to standard formats (CSV, PDF, structured backups), assistance in transition handover.

Red flag pattern: Long notice periods (90+ days), termination fees, "proprietary" data formats that only their software reads, no transition support clause.

Question 5 — What's your financial close and audit cadence?

A monthly close means the books are reconciled and reported on the same calendar rhythm every month. A quarterly close means there are three months a year where nobody knows what's actually in the accounts. An annual close means you find out about discrepancies eleven months after they happen.

The audit cadence is a separate question. Audits are external, conducted by a CPA firm, and run on annual or biennial cycles depending on community size and state requirements. A management firm that resists audits is a management firm with something to hide.

Good answer pattern: Monthly close on a published rhythm, annual external audit support, willingness to discuss findings from prior audits.

Red flag pattern: "Quarterly close" (industry-standard, but a sign the firm doesn't have continuous financial intelligence), resistance to external audit, vague answers about audit findings.

Question 6 — What does the board portal actually show, and who has access?

A board portal is the digital surface where board members see what's happening in their community. The quality of the portal is a strong proxy for the quality of the firm's operational systems. A firm with thin operational systems can't build a useful portal because there's no real-time data flowing into it.

Ask to see a live demo of the portal, with actual community data (anonymized if needed). What does the financial summary look like? Can you see maintenance status without asking the manager? Are vendor performance metrics visible? Does the portal update in real time or is it a quarterly snapshot?

Good answer pattern: Live demo offered, real-time data visible, role-based access (board sees more than homeowners), mobile-friendly.

Red flag pattern: "We email the board reports each month" (which means there is no portal), demo refused, login screens with no live content behind them.

Question 7 — Who owns the compliance calendar?

The compliance calendar tracks the operational obligations that have hard deadlines: statutory filings, insurance renewals, audit windows, board cycle elections, CC&R review intervals, vendor certification expirations. Some are state-level. Some are county or municipal. Some are tied to the community's specific governing documents.

The question "who owns the compliance calendar?" reveals whether the firm has one. The right answer is a specific role — "our administrative manager runs a twelve-month forecast that's reviewed monthly" — not a vague "we keep track of all that."

Good answer pattern: Named role or system, defined cadence, ability to show the calendar in a meeting.

Red flag pattern: "We have it covered" / "Our team handles compliance" / any answer where nobody specific is accountable.

Question 8 — How do you handle insurance renewals?

Insurance renewals are the moment most HOA boards realize how much the management firm has been doing or not doing on their behalf. A firm with operational depth tracks every policy's renewal date, surfaces the renewal sixty days before the deadline, runs a market check, and comes to the board with options.

A firm without operational depth waits until thirty days before renewal, accepts the incumbent carrier's quote, and tells the board "the new premium is up twelve percent — let me know if you want to approve it." The board approves because there's no time to do anything else.

Good answer pattern: Sixty-plus day lead time, market check process, multiple carrier quotes presented, clear recommendations with reasoning.

Red flag pattern: Reactive renewal posture, single-carrier relationship, "we use whoever the firm uses for everyone" (which often means the firm has a referral relationship with one broker).

Question 9 — What's included in board meeting support?

Some firms charge per meeting. Some include unlimited meetings in the base management fee. Some include "regular" meetings but charge for special meetings, executive sessions, or homeowner-attended sessions.

The question matters because board meetings are where the actual governance happens. A firm that meters meeting support is a firm that's signaling meeting work isn't part of their core service. That's a structural issue, not a pricing one.

Good answer pattern: Unlimited meeting support, including special and executive sessions, included in the base fee.

Red flag pattern: Per-meeting fees, caps on meeting count, charges for after-hours meetings or executive sessions.

Question 10 — Walk me through a transition runbook.

The last question is the most diagnostic. Ask the firm to describe, step by step, what the first ninety days of working with them looks like.

The good answer is detailed, named, and rhythm-driven: "Day one we activate the homeowner portal and ingest your historical financials. Day fifteen we complete a compliance audit and surface any urgent items. Day thirty we run the first board meeting under our facilitation. Day sixty we publish the first monthly close. Day ninety we conduct a transition review with the board."

The bad answer is vague: "We work with you to make sure the transition goes smoothly." That's not a runbook. That's a sentence.

Good answer pattern: Named steps, named dates, named owners, named outputs.

Red flag pattern: "We tailor the transition to your community" (which means there is no standard runbook), no specific timeline, no defined deliverables.

How to score the answers

The ten questions don't need a numeric scorecard. They need a recognition pattern.

After ten questions, you should be able to answer one bigger question: does this firm have an operational rhythm, or are they running on personality? Firms with rhythm answer the questions in the same shape — specific cadence, named roles, defined outputs, willingness to show the work. Firms running on personality answer the questions with reassurances, anecdotes, and "trust us."

You're not hiring a personality. You're hiring an operating model. The personality wears off in six months. The operating model determines whether the next three years go well.

If a firm answers seven or more of the ten questions with operational specifics, they're worth a closer look. If they answer five or fewer with specifics, they're a firm running on relationships and hoping operations don't trip them up.

What this framework reveals about Core HOA

We built Core HOA's operational rhythm around the same questions every board should be asking. Continuous monitoring, monthly close, twelve-month compliance calendar, transparent vendor pass-through, full data export on exit, and a published transition runbook.

The intelligence layer that runs underneath our service makes the operational answers possible. Daily data ingestion feeds monthly closes. Monthly closes feed quarterly intelligence reviews. Compliance calendars get tracked on the same rhythm whether the community has thirty doors or three hundred. The math behind every answer in the framework above is the math we run for every community we manage.

For boards evaluating Core HOA against other firms, the ten-question framework should produce a clear comparison. We answer ten of ten with operational specifics — including the questions about exit terms and vendor markup that most firms duck. The framework is also a fair test of whether we're the right fit. If a board asks the ten questions and gets better operational answers from a different firm, hire them. The point of the framework is to make the right call, not to make the call for Core HOA.

Frequently asked questions

What questions should an HOA board ask before hiring a management company?

The ten questions above cover the operational reality: response SLAs, reserves visibility, vendor markup policy, exit clauses, financial audit cadence, board portal access, compliance calendar ownership, insurance renewal handling, meeting support scope, and the transition runbook. Most firms can answer four or five well. The ones that can answer all ten are the ones worth hiring.

What are red flags when evaluating an HOA management company?

Vague response time commitments, hidden fees on top of the management rate, vendor markups the firm refuses to disclose, exit clauses that hold your data hostage, and any answer that includes the phrase "we'll handle it" without explaining the actual mechanism. If a firm can't show you their compliance calendar or describe their close cadence, they don't have one.

How long does it take to switch HOA management companies?

A clean transition runs 60-90 days from contract signature to full operational handover. Anything faster usually means corners are being cut. Anything slower usually means the outgoing firm is making the handover difficult, which is itself a sign the board made the right call to switch.

Should an HOA hire a local management company or a national firm?

Both can work. National firms bring scale and standardized systems but often dilute attention across portfolios. Local firms bring direct accountability but vary widely in operational depth. The question that matters more than local-versus-national is whether the firm has the operational rhythm to catch problems before they become assessments.

How much should an HOA management company cost in Utah?

Utah HOA management fees typically run $15-$50 per door per month, depending on community size, service scope, and whether ancillary fees are bundled or itemized. The sticker price matters less than the total cost of ownership including hidden fees, vendor markups, and the cost of operational gaps the firm doesn't catch.

Evaluating Core HOA?

If you're shopping management firms, run the ten-question framework on every firm you talk to — Core HOA included. We'll send the math, not the marketing.

Marc Kennedy is the owner of Core HOA, a family-owned HOA management firm based in Cottonwood Heights, Utah. Core HOA has managed Utah communities for over twenty years across the Wasatch Front. Marc reads every email sent to marc@corehoa.com.